Flat-rate farmers got €66m back in VAT refund claims in 2025

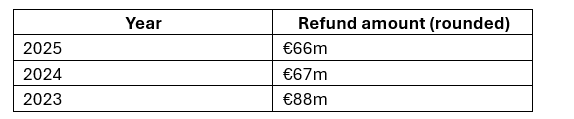

Revenue refunded over 27,000 "VAT 58 refund claims" totaling €66 million to flat-rate farmers last year according to latest figures.

But the 2025 refund total was significantly down on the refund total just a year earlier - which finished at €67 million for 2024 and also compared to the amount paid out in 2023 on VAT refund claims.

According to Revenue no breakdown is available in relation to the specific areas of spending on which the refunds were issued.

The VAT Flat Rate (FFR) scheme is for farmers who are not registered, or required to register, for Value-Added Tax (VAT).

These farmers are commonly referred to as flat-rate farmers. The majority of farmers are not registered for VAT.

These farmers are allowed to add and retain a percentage charge - known as the flat-rate addition - onto the amount they invoice VAT-registered businesses who they supply with agricultural goods and services, including livestock, in the course of their farming business.

The level of the flat-rate addition is calculated in accordance with the EU VAT Directive, is reviewed annually and is set out in Irish VAT legislation.

The flat-rate addition was 5.1% in 2025.

In Budget 2026 it was announced that the farmer's flat-rate addition would fall to 4.5% from January 1 this year.

Flat-rate

Generally, flat rate farmers cannot deduct VAT on their business costs.

According to Revenue VAT can only be refunded to unregistered farmers in relation to costs incurred:

- For the construction, extension, alteration or reconstruction of that part of farm buildings or structures;

- For the fencing, drainage or reclamation of any farmland;

- For the construction, erection, or installation of qualifying equipment for the purpose of micro-generation of electricity for use solely or mainly in a farm business.

Farmers must submit claims for repayment on Revenue's form VAT 58.

Under current Revenue rules farming structures are "man-made structures that are fixed to, or in, the ground and which cannot be easily dismantled or moved, such as farm roads, farmyards, and silage pits".

Certain types of equipment - such as automatic calf feeders - do not qualify for a VAT refund.

From September 1, 2025, broiler chicken services have also been excluded from the FFR scheme.